Summarise the key points discussed in the episode?

Were there any notable quotes or insights from the speakers?

Which popular books were mentioned in this episode?

Were there any points particularly controversial or thought-provoking discussed in the episode?

Were any current events or trending topics addressed in the episode?

What was the main topic of the podcast episode?

Summarise the key points discussed in the episode?

Were there any notable quotes or insights from the speakers?

Which popular books were mentioned in this episode?

Were there any points particularly controversial or thought-provoking discussed in the episode?

Were any current events or trending topics addressed in the episode?

About this Episode

Dr Mike Jones, the Managing Director of Impact Minerals Limited (ASX: IPT), is talking about a Western Australian High Purity Alumina project in a Coffee with Samso 175.

The HPA (High Purity Alumina) story has so far eluded the Samso journey. but nowImpact MineralsLimited(ASX: IPT)is sharing. The HPA story require an understanding of a whole different pool of facts.

Although the HPA story is not something new, it does bring a whole different complexion to Impact Minerals. If you hear Dr Mike Jones describing the story, you may feel that this is a simple project.

You are not wrong, but to me, it is far from simple but this is one of those projects that is niche enough to make it work.

Impact Minerals is now embarking on a different journey. This new project is almost ready for the production story. They are finalising the drilling to produce the all important JORC Mineral Resource which will be the first step in cultivating a production story.

Get to know Impact Minerals Limited (ASX: IPT)

Impact Minerals have been around for a long time. Impact is a company that has projects that would a major project in any other ASX companies. The Broken Hill and the Arkun project especially.

The Broken Hill project is a Ni-Cu-PGE project (Figure 1 and Figure 2) is located with 20km from the world class Broken Hill silver-lead-zinc mine in New South Wales.

The geology at the Broken Hill project is one that has a lot of possibilities which is what you want from a project. I have looked at their projects from afar for a while.

Figure 1. Location of the Broken Hill Ni-Cu-PGE Project. (Source: Impact Minerals Limited)

Impact has shown that the very high grade palladium and platinum mineralisation at the Red Hill, Platinum Springs and Moorkaie Prospects and the Iron Oxide Copper Gold (IOCG) mineralisation at the Copper Blow Prospect (ASX:SCI) are hosted by and related to alkaline magmatic rocks (Figure 2), (ASX Announcement13th December 2018).

Figure 2: Location of alkaline magma trends in the Broken Hill area. The Little Broken Hill to Moorkaie Trend contains rocks of potassic ultramafic to alkaline gabbro composition. The Copper Flat to Staurolite Ridge Trend contains rocks of alkaline gabbro to carbonatite composition. An offset of the Copper Blow Trend is interpreted to the south of the Thackeringa Fault Zone. (Source: Impact Minerals Limited)

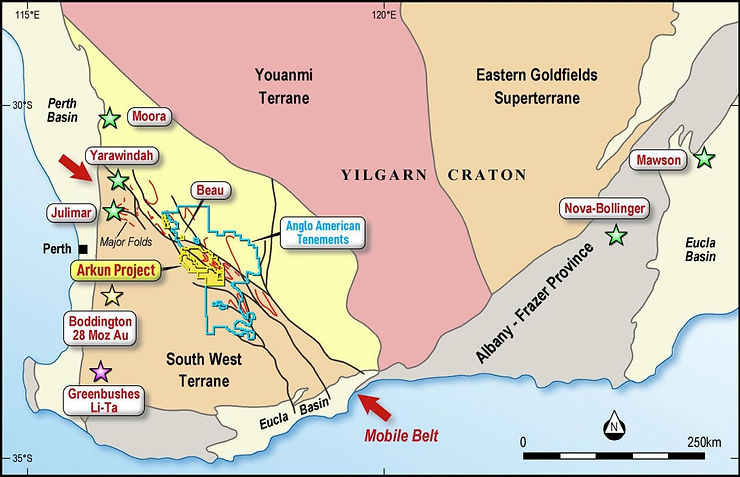

The Arkun project (Figure 3) which covers about 850 square kilometres is between York and Corrigin, which is approximately 100 km east of Perth. The project was first identified as an area of anomalous nickel-copper-gold anomalies in publicly available regional geochemistry data sets.

What I like about this project is that it is now considered to be in a mobile belt that is prospective for "Julimar" type mineralisation. The discovery of Julimar has now opened up this whole region.

Figure 3: Location and Regional Geology of the Arkun Project and showing key nickel-copper-PGE deposits and recent discoveries. (Source: Impact Minerals Limited).

A subsequent interpretation of regional magnetic data by Impact has identified the area as lying within a major deformation zone ormobile beltthat trends NW-SE from the Moora-Julimar-Yarawindah area through Arkun and which may contain deformed and metamorphosed equivalents of those rocks .

This belt is generally not recognised in many regional geology maps and yet is self-evident in the magnetic data. This is a significant breakthrough in understanding for Impact.

The BHP Xplore Program

Impact Minerals was recently chosen to participate in the BHP Xplore program with their Broken Hill project. The participation is a recognition of the quality of the project and the amount of good work completed by the company.

Think about the amount of projects that would have been submitted and to be selected is a testament of something positive.

The Lake Hope HPA Project will change the future of Impact Minerals Limited.

The Lake Hope Project covers numerous prospective salt lakes between Hyden and Norseman in southern Western Australia ,a Tier One jurisdiction (Figure 4). The project covers about 238 sqkm and are all owned by the vendor, Playa One.

Figure 4: Location of the lake Hope project.

The Lake Hope area has unique climatic and geological characteristics that have resulted in the formation of what is probably a globally unique deposit of aluminium-rich material within the surficial clay layers of two small salt lakes, or “pans”, in the Lake Hope playa system.

The lake clays, which are only up to a few metres thick, have unique chemical and physical properties and consist almost entirely of aluminium-bearing minerals that are plasticine-like in consistency and can be easily sampled with hand-held augers and push tubes (Figure 5).

Figure 5: Lake Hope showing the push tube sampling method (!) and an example of the lake clay from the push tube. (Source: Impact Minerals Limited)

In addition, particle size distribution analysis demonstrates that virtually all the minerals are less than 16 microns and 60% to 80% occur at grain sizes of less than 5 microns (Figure 6).

Figure 6: Particle size distribution analysis for four samples. Sample LP0040 contains sandy particles at the base of the deposit. (Source: Impact Minerals Limited)

These unique characteristics have produced a near-perfect mineral deposit: a very high-value end product whose parent ore is:

Very soft and shallow, allowing for extremely cheap free-digging with limited infrastructure requirements, no pre-stripping, no selective mining, a tiny environmental footprint, and limited rehabilitation requirements.

Naturally fine-grained with no need for crushing and grinding, allowing for transport to an offsite processing facility that can be built on existing industrial sites (Figure 4). In essence, this is Direct Shipping Ore (DSO).

Comprised of a few minerals that require only simple washing before acid leaching, thus allowing for low-cost straightforward metallurgical processing.

Samso's Conclusion

The change in business for Impact makes a lot of sense. The introduction of the Lake Hope project will move Impact Minerals into the production part of the industry very quickly. As we all know, in the exploration game, discovery of an economical resource is very difficult. The path to production is another hurdle many small juniors will never cross.

What I like with Impact are their "Other" projects. There is a lot I like about the new HPA label. However, one cannot discard the potential of the Broken Hill and also the Arkun project. There is hard to measure value in the potential of these projects.

I have always considered the HPA as too hard. However, now listening to Mike sharing his thought and strategy with the Lake Hope project, I am changing my narrative. To be honest, I have not really looked into the details but I have got some idea now.

Simplistically, the HPA story appear to be about processing. The mining part seem to be easy. This is what I take away from listening to Mike and his confidence, I feel, comes from the fact that Lake Hope is a unique deposit. It is one of those projects that tick the boxes that we all dream about.

When you look at this project, Lake Hope, what I see is that, at this stage of the game, Impact has been lucky. They got this project which appears to have all the hallmarks of a "Perfect Project". Yes, we all know about the things that can and will go wrong with the path to production, but I think when you listen to Mike speak about the ups and downs, you will come to the same thought Could this be true?

When the time comes where we get the answer to that question, I would rather be the group that have the position to lose than the group that is fighting for a position. My philosophy has always been that I rather lose something than regret not being able to win. Welcome to the Mineral exploration game..... DYOR.

Tune in to Mike's thoughts here.

Chapters:

00:00 Start

00:20 Introduction

01:37 The Impact Minerals Limited story

06:28 HPA - Potential big player in the industrial minerals market

09:19 The deposit and metallurgical process of extracting HPA

12:13 What is special about the Lake Hope Project?

18:49 The assay results in Lake Hope

21:15 What is 4N high purity alumina?

23:50 Advantages and challenges of the alumina deposit

28:07 The chemistry consistency of alumina grades

31:27 The competitive advantage of Lake Hope area

32:45 The challenges of being in the HPA space

35:06 A low cost producer of HPA

37:29 News flow

40:29 The advantage of leapfrogging the discovery phase

As we close off 2023, what a better way to end with Coffee with Samso Episode 193 is with Brett Hazelden, Managing Director and CEO ofOD6 Metals Limited (ASX: OD6).

The Rare Earth story is now reaching a stage where it is now all about the chemistry. Most followers of the sector are now assuming and accepting that companies will report minerals resources that will be large enough to sustain any operations.

What is unknown is the cost of the chemistry that will bring in the revenue and profits at the end of the exercise. I think in this episode of Coffee with Samso, Brett Hazelden makes a very compelling case for the OD6 Metals story. There is a lot of confusion in the market in terms of what is the end game for these clay rare earth projects.

Brett is a metallurgist and he comes from experience when he talks about the downstream process. For those viewers who are pondering about the Rare Earth sector, this is a must watch episode of Coffee with Samso.

Samso Conclusion

As many of you who have followed the Samso platform, you would have been watching a lot of Rare Earth stories lately. There is no doubt that the rare earth industry is very complicated and confusing which is primarily being fuelled by a cloud of uncertainty on the future. This is something that I had as well but you would have heard me mention this very often, recently, that the trip to the rare earth conference in Canberra has pretty much cleared it up for me.

My optimism that was derived from the conference is not an indication that the sector is going on a bull run. My thoughts are that the reality of a strong future for the demand of rare earths will be very profitable for the companies that stick to their work and are able to sustain their path with funding.

The ability to attract funding over the period is critical. In some ways, you could look at the this time of the market as a reset of the rare earth story, in terms of valuation. This is the time to do your DYOR. For all investors, if the commodity boom is around the corner and the rare earth metals are part of that run, then you would want to do some good research now.

Chapters:

00:00 Start

00:20 Introduction

01:03 2023 recap

03:32 Understanding the chemistry

07:14 Lowering the costs of production

09:45 Discussion about ESG

11:27 What is driving the economics of these clay projects?

15:46 Difference between Australia and South America - grade and processing route?

19:38 Takeaways from the Canberra REECon

26:16 What’s on the cards for 2024?

32:03 Discussion about the rare earth market price

Coffee with Samso 192 has Andrew Radonjic talking Rare Earths at the Jupiter project.

Venture Minerals Limited (ASX: VMS)is now at the crossroads of emerging as a Rare Earth player in what is a complex and ultimately future-proofing sector. I labeled Venture Minerals as aTargeted Diversified Mineral Explorerin my very first interview with Andrew Radonjic, the Managing Director way back in October 2020, and this is another prime example of that business approach.

The rare earth sector has had a lot of attention in the last 24 months and like all commodities, it is going through turbulent times. Samso has had the greatest privilege to have interviewed many of these stories over time and I see Venture Minerals as an interesting change to the current scene

On the back of the recent announcement by Venture Minerals on the 29th of November 2023, entitled Jupiter Delivers over 7,000 ppm TREO assays from Maiden RC Drill Program, the company has raised additional funding to work on the project. In the current market, this is a strong vote of confidence for the potential of the Brothers REE project.

In this episode, Andrew Radonjic shares with us his thoughts on the project and a good insight into the facts of the recent drilling results. In combination with the historical exploration activities, the picture of why Venture Minerals feels this project will have a future is material for viewers.

Check out the conversation with Andrew Radonjic below:

Samso's Conclusion

As I have mentioned, we have had a good amount of content that is related to the rare earth sector, and my thoughts, which are consistent with most commentators, is that every REE project is unique. The key is what is at the bottom line of the project. Does it make money when the cookie crumbles?

The Jupiter target is a clay-hosted rare earth project and as Andrew mentioned, there has been little metallurgical work done but these days, we are very comfortable assuming that it is a typical clay-hosted ree system. I don't think that this is a unique clay-hosted system but what will make it different is the logistical and the potential grade and tonnage.

The other point of difference is a different social license. Most of the other projects have to deal with private landowners and the existence of the population. It may not be obvious now but I think in the long run, the bottom line will be noted.

This is not to say that the others will not make money. As I measure the landscape for this sector, the companies that are left standing in the long term will be big winners. Fresh investors with more money in the bank will go a long way to becoming a long-term player.

Chapters:

00:00 Start

00:20 Introduction

00:54 What is happening with the Jupiter REE Target?

03:56 Does alkaline intrusion play a part in Jupiter?

06:50 Progress on the drilling at Jupiter

14:11 What sets VMS apart from the others?

25:17 Comments for existing shareholders

29:37 Why did the recent new investors buy into the VSM Story?

I have always said that Richard Brescianini, the Executive Director of Heavy Rare Minerals Limited, is the best person when it comes to understanding how the Rare Earth sector functions. Richard has had decades of experience within the sector and in this Coffee with Samso, he shares with us what is happening with HRE and what is the path forward in 2024.

The rare earth sector is undergoing some reality checks and as investors look around, there are only a real handful of companies left that can be considered as real contenders. There is a rush to go to Brazil to chase the so-called "ionic" projects but what everyone has to consider is what will be the economics of the business.

In this episode, Richard and I discuss what makes the business work. The metal extraction is critical and we know the answer is acid. The more acid we use, the more metals we get out. The cost of the acid extraction is a big hurdle but don't forget all the other aspects of the business.

Australian Clay Rare Earth projects may appear to be lacking in properties that are beneficial to having a good REE project, but they have lower jurisdiction risks, and hence the cost of having a sustainable infrastructure becomes challenging. Projects need to have consistency in all aspects of the deposit, such as metallurgical factors and grade.

We also discussed the other projects such as Duke and Perinjori. There was some exploration news on Duke and we had a good discussion on the merits of the project.

Samso's Conclusion

This Rare Earth sector requires investors and companies to have a long-term view of commercialisation. We all know that the challenge in working on clay rare earth projects has been a long road and very challenging. There have been many comments that the outcome for the companies promoting these projects will end in tears. If you have been following the markets you will be swayed with the depressed equity market.

I must admit that I had similar thoughts. My thoughts are whether the demand and the hype would be sustained. I recently attended a Rare Earth Conference in Canberra and I was surprised that I was super attentive over the 3 days. I think I may have only missed one talk. What I took away from that conference was a renewed enthusiasm for the sector.

The main reason is that there appears to have been a lot of money already spent. Furthermore, there seems to be a lot more money that is in place to help create a new downstream chain that is outside China. Before going to the conference, I heard all the talk but one has to take all those noise with some caution.

However, after the conference, I am convinced that the talk is real and the demand for more REE is believable. The establishment of the downstream process is in no way near being completed but the process is there. The amount of money that has been pledged to establish a non-China-aligned downstream chain is staggering. The projected demand for REE for our electrification journey appears to ensure the longevity of companies such as HRE.

Hence, my opinion for those who are interested in this sector should DYOR and look into what is happening behind the noise you hear from the general stream of news. Spend some time and look into what is happening in the real REE world.

Chapters:

00:00 Start

00:20 Introduction

01:10 Cowalinya Exploration Target

06:03 Could the geology create issues for your Exploration Target at Cowalinya?

09:05 All about the Duke Project.

14:03 Do you think Duke could have a different REE chemistry?

17:24 New Project - Perenjori

22:32 Discussion about the clay-hosted space

27:21 A second supply chain for the rare earths market?

37:58 What are the immediate goals for HRE to monetise the business?

Coffee with Samso Episode 189 is with Mike Haynes, Managing Director and CEO of New World Resources Limited (ASX:NWC).

The last time we spoke toNew World Resources Limited (ASX:NWC)the story was about getting mining happening. Today, we hear that the mining process is in place and while they are going through the paces, they are chasing very compelling exploration targets.

There are very few to no stories on the Australian Stock Exchange (ASX) that is flavoured copper not to mention high-grade copper. The Antler project by all accounts in the copper mineral exploration industry is a technically strong project. It is probably better categorised as a near-producer story now as the company moves into the mine planning stage.

Samso's Thoughts

New World Resources, as I have stated earlier, is a no-brainer for making a strong DYOR company on your watchlist. The bearish sentiment in the market which has depressed equity pricing in the small-cap sector is a blessing in disguise for new players into New World Resources.

For existing shareholders, it may be a good time to average down. I remember myCoffee with Samso with Rick Rule (Commodities and Equities: Advice from Rick Rule - Episode 70)where he talked about the story of when he had bought Paladin Energy Limited (35:54Rick and Paladin - The story of Investing in Mineral Explorers) all the way to 1c because he believed in his own conviction of the quality and the factual truth of the project and the company management.

For those people who sat through all the Coffee with Samso episodes with Mike Haynes, you would see the consistency of the conversation. The technical aspect of Antler is rare in this industry. TheGolden Grove VMS depositin Western Australia would be something that Antler should be compared to, in terms of technical attributes and potential.

For those people who are entertaining the idea of learning more about New World Resources, please feel free to send me an email and I will forward it to Mike Haynes. I strongly encourage dialogue with management as they are more than happy to take the time to go through your queries.

Check out this Coffee with Samso with Mike Haynes from New World Resources Limited.

Chapters:

00:00 Start

00:20 Introduction

01:15 Updates from New World Resources

02:24 The resource value

03:17 Upsides to the Antler exploration

05:33 Discussion about the recent scoping study

08:07 Discussion about Porphyries

10:36 The mining strategy

14:30 VMS belt clusters

20:16 The Javelin Project

23:48 The next set of drilling

27:45 Discussion about current commodities

30:20 Exceptional IP anomalies

37:29 Any possible risks?

40:34 News flow

43:38 Why should investors look at New World Resources?

The journey to understand the ins and outs of the Rare earth sector has been sparse over the last two years. The sudden rise of the REE sector is a perception that has been shrouded with a lack of understanding.

Samso's Conclusion

Heavy Rare Earths Limited is slowly ticking the boxes to go towards producing a Rare Earth product which will ultimately bring revenue to the company. The upgrade of the Mineral Resource has effectively allowed HRE to show that they have the means to be a major player.

Richard Brescianini has made it very clear that the final grade going into the plant will be Tier 1. Richard is one person who has seen all the issues and he will be able to see the hurdles coming for all the players in this sector. His experience will be the critical measure when HRE travels down the line of finding buyers for their product.

This Coffee with Samso has some very important thoughts from Richard and I recommend proponents that want to learn the business end of the REE sector, get comfortable and settle in for a lesson.

Chapters:

00:00 Start

00:20 Introduction

01:07 Richard update

03:08 An upgrade in resource and grade.

06:21 A natural mineralisation cut-off.

06:47 What investors need to understand about resource grade and mill grade.

07:43 Are there more high-grade pods in your project?

12:03 Grade/Thickness and Grade/Tonnage Curve

17:08 Is there a sweet grade spot in the project?

19:06 Metallurgical Flow Sheet

20:21 New metallurgical drilling samples.

21:37 Aim to produce a mixed REE carbonate for potential customers.

22:27 Giving reasons for potential customers to invest in HRE.

22:59 Strategy to Brand HRE to potential customers.

24:21 Branding HRE as a real REE producer.

25:46 The market of REE, the upside, the current price of REE, and why it's rising.

29:25 What is the sweet sustainable price for REE?

30:38 Upgrade in Mag REE for HRE.

31:29 The importance of Magnetic REE.

32:39 Recovery results tend not to change very much.

In this episode of Coffee with Samso 188, we have David Groombridge, CEO ofRiedel Resources Limited (ASX: RIE)sharing with us an update on Exploration activities at the Kingman Project.

The Riedel Resources story is one of the few real exploration plays on the Australian Stock Exchange (ASX). In this episode of Coffee with Samso, David Groombridge gives us a quick update on the project and what shareholders and potential investors should be looking out for in the coming months.

Listen to our coffee conversation with Mike Bohm and David Groombridge here:

Tune in to the Riedel story here.

Chapters:

00:00 Start

00:49 Update from David Groombridge.

01:22 Any new Learnings at The Kingman project.

02:24 The Tintic - Jims Structural Corridor.

03:19 Any resemblance to Mineral Park?

05:04 What is the Exploration strategy now?

06:25 Exploration is a long-term proposition.

07:32 Any issues with regulatory issues?

08:04 What would make Investors worry and celebrate the Riedel story?

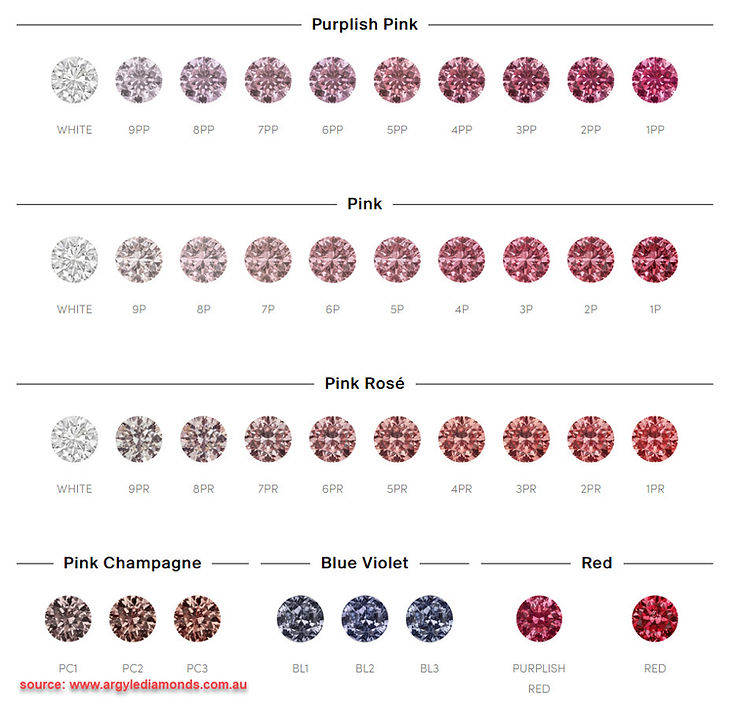

n terms of a significant mineral discovery in Australia, one cannot go past the search for the Argyle Diamond Mine in the Kimberley Region of Western Australia. The Argyle Diamond Mine discovery was the first of its kind in every aspect of the project.

Episode 115 of Samso Insights is all about Ewen Tyler and how he narrates a discovery of a lifetime.

Ewen Tyler is the man who is credited as the "Father of the Argyle Diamond Mine". I will have to say that as much as all Discovery Journeys is a team game, there had to be a driver and a man to take the heat.

The diamond project was the biggest, had the best grade, was the first major diamond deposit discovery in Australia, and most importantly, it was the first diamond discovery outside the cartel of De Beers and the Russian Federation.

A History of the Argyle Diamond Mine

(Wilipedia)

TheArgyle Diamond Mine (Figure 1)was adiamond minelocated in the EastKimberleyregion in the remote north ofWestern Australia. Argyle was at times the largestdiamondproducer in the world by volume (14 million carats in 2018[1]), although the proportion of gem-quality diamonds was low. It was the only known significant source ofpinkandreddiamonds (producing over 90% of the world's supply), and additionally provided a large proportion of other naturally coloured diamonds, including champagne, cognac, and rare blue diamonds.

Mining operations ceased in November 2020, after 37 years of operations and producing more than 865 million carats of rough diamonds. Mine operatorRio Tintoplans to decommission the mine and rehabilitate the site at least through 2025.[2][3]

The Argyle diamond mine is also notable for being the first successful commercial diamond mine exploiting avolcanic pipeoflamproite, rather than the more usualkimberlitepipe; much earlier attempts to mine diamonds froma lamproite pipeinArkansas, United States, were commercially unsuccessful. The Argyle mine is owned by theRio Tinto Group, a diversified mining company that also owns theDiavik Diamond Minein Canada and theMurowa diamond minein Zimbabwe.

Figure 1: The Argyle Diamond Mine.

Argyle _ The Impossible Story of Australian Diamonds","target":"_blank","rel":""}}},"VERSION":"9.14.3"}">

My Fascination for Diamonds and Diamond Exploration

This episode of Samso Insights will go down as one of my favorites. It was a great privilege to have had access to a story like that of Ewen Tyler. The greatness of his achievement is his ability to keep the search for a diamond source alive for so long. I have been a big fan of diamond exploration since I started my Honours Thesis at the University of Western Australia.

In fact, if my memory serves me correctly, I had a great interest in gems even before my time at University. As Ewen put it perfectly, "Only Fools Will Explore for Diamonds". This statement is in fact very common with people who have had the taste of diamond exploration. It is probably safe to say that only passionate explorers will appreciate the hardship that diamond explorers had to go through with little to no reward.

There is not much to elaborate here except to tell readers to settle in and listen to what is arguably one of the best stories about persistence and gamesmanship to persist with the search for a "potential" diamond discovery.

The interview has been largely guided by the book by Stuart Kells entitled " Argyle - The Impossible Story of Australian Diamonds". When I did the Samso Insight about the discovery of the Olympic Dam, I did not have the information about the business side of the process. This book by Stuart Kells gave a great narrative on the Boardroom aspect of the journey.

To Purchase the book click on our Amazon Affiliate link:

The diamond exploration industry is pretty much non-existent today. I think there is one company that may be active in the industry worth mentioning. The industry is now all about the existing miners as the flare of exploration is now too expensive. In the business of mineral exploration, the risk-reward ratios are now not even worth discussing.

The Arglye story is inspired by the famous pink diamond but as Ewen Tyler spells it out, there was no consideration of these stones. The success of Argyle was the marvels marketing the value of the stones which made the mining process work.

In my opinion, there is nothing more beautiful than a good coloured stone (Figure 2). There will be many narratives out in the public space that will argue that a quality white will forever be better, but a beautiful stone is one that makes a statement. It is about what the stone shoes and the history that it comes from that creates the value. If you watch this interview, you will get the sense that the value of the argyle stones was all about the Argyle story.

Figure 2: A range of Argyle's best.

Chapters:

00:00:00 Start

00:00:15 Introduction

00:01:00 The Ewen Tyler Story - The beginning

00:13:02 Rex Prider Factor

00:14:46 Start of the search for diamonds in Australia

00:17:21 Introduction of Rio Tinto

00:18:22 Path to Ellendale

00:20:14 Business of Ellendale

00:20:52 Discovery of diamonds in Smoke Creek

00:21:25 Bringing context into the search area

00:22:16 Team Argyle

00:24:41 Arrangement with the Western Australian Government

00:28:27 The Rio Tinto Lifeline

00:29:42 Early signs of the discovery of Argyle

00:31:34 Waiting Game - The Process and The Secrecy Game

00:33:53 Ewen earned the title of The Father of Argyle Diamond Mine

00:37:02 Arriving at Argyle

00:38:05 Unbelievable Grade of Diamonds

00:39:43 Smoke Creek and Limestone Creek - First sighting of the Argyle Pink Diamond

00:40:42 The Mythical Value of the Pink Diamonds for Argyle

00:42:50 Economic Study of the Argyle Diamond Mine

00:43:17 Funding the mining of Argyle Diamonds

00:50:08 First Nation Discussions

00:53:47 The Birth of the Marketing Gunnies of the Argyle Diamonds

01:00:31 Webb Diamond Project

01:01:28 Other sources of diamond projects

01:03:49 Ewen Thoughts on Mineral Exploration

01:05:34 Importance of the Team in Mineral Exploration

01:07:04 Is there an Impossible Exploration Discovery?

Mount Ridley Mines is now focusing on the flow chart of the REE business. This is the money end, can you make the processing part cash flow positive?

When I had my first Coffee with Samso with Guy Le Page, in July 2022 (Mount Ridley Mines Limited (ASX:MRD) - A Rare Earth Story.), it became evident that the company had a strong focus on optimising its flow chart. The company was confident in its ability to achieve the desired tonnage and grade, but its primary emphasis was on the final stage.

In my view, one of the major benefits for companies like Mount Ridley is their project's location in the Esperance region. Numerous discussions have highlighted the region as the ideal site for the government to establish a Rare Earth Hub.

Check out the conversation in this Coffee with Samso and, as I always encourage, DYOR.

Chapters

00:00 Start

00:20 Introduction

01:10 Updates on the Mia Project

02:45 Beneficiation Results

03:55 Leach Test Results

04:59 Is Mia the main focus of Mount Ridley?

06:01 Mia prospect air-core drilling

06:37 Discussion about the soft REE market

09:05 Q&A from the public

09:19 Is MRD still going to list on the Frankfurt Exchange?

09:46 What is MRD’s strategic roadmap beyond 2023?

10:59 How is MRD taking a position for success amongst Esperance peers?

11:59 Is using HCL costly? And what about government grants?

13:03 Has MRD determined the controls in the clay-hosted REE project?

15:24 Prediction of the path of the REE market as we move forward

17:01 What makes MRD stand out?

18:20 Discussion about the REE market

20:17 Conclusion

Samso's Conclusion

When investing in the Clay Rare Earth sector, it is crucial to consider the economic viability of the processing flow sheet, and, while the industry has yet to determine its profitability, this does not mean it won't become a viable option. However, it is important to acknowledge that the industry is still in its early stages, and there will be a steep learning curve filled with uncertainty.

The industry has successfully identified the process of leaching out the Rare Earth Elements (REE), but the economic outcome in terms of profitability remains uncertain. The REE sector, including both hard rock and "Clay/ionic/alluvial" types, has gained attention in investment circles due to recent geopolitical developments.

China's dominance in this sector is widely recognised and understood. The previous discussion on REE in the investment community was short-lived in 2010, as the market experienced rapid fluctuations. However, the current rise of the REE sector has shown more resilience, having been present for a couple of years, largely due to the new "cold war" with China.

Balancing the REE sector will require time, and investors in this sector must cultivate patience, akin to the patience required for fishing. It is frustrating to continually emphasize that mining projects are measured in terms of years to decades, while investors, particularly new ones, expect quick results within weeks or months.

Unfortunately, such quick results are unlikely to occur. Regarding Mount Ridley, they have a solid strategy, and recent results indicate a viable business. However, the investment community needs to learn to be patient and learn to "PARK" their money.

In Episode 186 of Coffee with Samso, Dr Mike Jones, the Managing Director ofImpact Minerals Limited (ASX: IPT), educates us on the ins and outs of the HPA business.

The HPA (High Purity Alumina) story for Impact Minerals is now all about the economic process of making HPA. There are no longer any questions on the tonnage or the grade. In simple terms, the company is at the business end of the mineral resource sector.

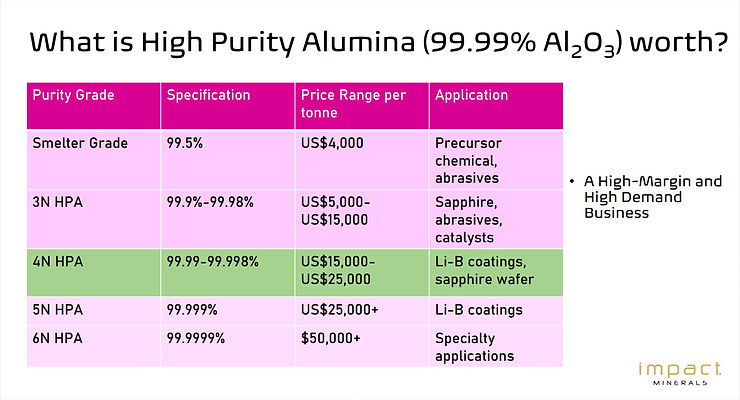

One of the key aspects of understanding Impact Minerals is to have a clear view of the company's business. Impact is in the business of HPA and what that means is that it needs to deliver High Purity Alumina in the 3N or 4N level (Figure 1).

When considering companies like Impact Minerals, the initial association is often with mineral exploration. However, it is important to view Impact from a fresh perspective. In this episode, Dr. Mike Jones discusses the company's current focus on the Pre-Feasibility Study (PFS) phase, which aims to determine the profitability of the Lake Hope HPA project. This shift in focus highlights Impact's commitment to reaching a stage of financial success, distinguishing it from the negative reputation often associated with mineral exploration companies.

Samso's Conclusion

Impact Minerals is a company that often goes unnoticed despite its promising projects. Currently, they are actively promoting the Lake Hope project, which has been discussed extensively by Mike during the past two Coffee with Samso sessions. It is evident that the Lake Hope HPA project holds significant value for the company.

It is worth mentioning that Impact Minerals' Broken Hill project was among the six projects worldwide selected for the prestigious BHP Xplor program. On17th of January 2023, the company issued a release providing further details about their participation in theBHP Xplor program.

BHP Xplor, an accelerator program introduced by BHP in August 2022, is designed to help provide participants with the opportunity to accelerate their growth and the potential to establish a long-term partnership with BHP and its global network of partners.

Impact received up to US$500,000 in cash payments from BHP over the next six months and gained access to a network of internal and external experts to help guide development in the technical, business, and operational aspects of the company.

This means that the management of Impact demonstrated credibility by successfully participating in and gaining acceptance for theBroken Hill project. This is a significant achievement, as only six recipients were chosen for this program, indicating a high level of quality.

While the market trader may perceive Impact Minerals' market capitalisation of 34.37M as high, there is an underlying value that will yield positive results in the future. The Arkun project, which we discussed in a recent episode of Coffee with Samso, is located in a jurisdiction occupied by Tier-1 resource companies like Anglo-American. This provides strong evidence of its prospectivity (Figure 2).

The Lake Hope projectis currently in the "Feasibility" stage, and the initial excitement surrounding it has diminished in the market. However, this does not undermine the value that Impact Minerals is creating for its shareholders.

There are two aspects of Impact Minerals that I appreciate. Firstly, the Lake Hope project is undeniably the company's flagship at the moment. Secondly, there is potential for significant growth from the Arkun and Broken Hill projects.

Tune in to Mike's thoughts here.

Chapters:

00:00 Start

00:20 Introduction

01:20 Updates from IPT

02:16 Economical parameters that make an HPA project viable

05:56 All about High Purity Alumina

07:54 The Cost Curve Analysis

11:23 Discussion about entry into the HPA market

12:43 The HPA space after the commodity market softening

14:07 The market for HPA

16:04 The Arkun Project

20:51 The Forward Plan

24:52 Is Lake Hope is still the Perfect Orebody?

25:33 How should investors view Impact?

26:55 Why should investors believe that Impact will deliver the end story?

29:00 With the current interest rate trend, is it a good time for companies like Impact Minerals?

30:55 Why should investors invest in Impact Minerals?

Coffee with Samso Episode 184 is with Julian Ford, CEOofRiversgold Limited (ASX: RGL)updating us on Riversgold's exploration activities since the last conversation inMarch 2023.

In our previous conversation, we discussed Riversgold Limited as a lithium explorer that I found interesting. One of the reasons I liked them is because they were among the few companies actively engaged in genuine mineral exploration for lithium. It's important for people to understand that the recent discoveries in the lithium sector have largely come from reevaluating previous exploration efforts. Companies have revisited their drill cores and discovered that the historical drilling had indeed encountered pegmatites.

Samso is not begruding of the success of these companies, such as the Mount Holland Lithium project, which is now privately owned and operated byCovalent Lithium. Riversgold, on the other hand, continues its exploration activities in search of valuable lithium-bearing pegmatite.

What I find interesting about Riversgold is their Northern Zone project. When I was researching this topic, I initially found their release titledFarm-in to Significant Porphyry Hosted Gold Projecta bit confusing because the project had yielded promising results.

The company is proceeding cautiously to ensure the reliability of these results, which I believe demonstrates prudent management. Julian, in particular, discusses the project and takes a measured view of its potential.

The major products from porphyry copper deposits are copper and molybdenum or copper and gold. The term porphyry copper now includes engineering as well as geological considerations; It refers to large, relatively low-grade, epigenetic, intrusion-related deposits that can be mined using mass mining techniques.

Geologically, the deposits occur close to or in granitic intrusive rocks that are porphyritic in texture.

There are usually several episodes of intrusive activity, so expect swarms of dykes and intrusive breccias. The country rocks can be any kind of rock, and often there are wide zones of closely fractured and altered rock surrounding the intrusions.

As is described following, this country rock alteration is distinctive and changes as you approach mineralization. Where sulphide mineralization occurs, surface weathering often produces rusty-stained bleached zones from which the metals have been leached; if conditions are right, these may redeposit near the water table to form an enriched zone of secondary mineralization.

What is the significance of a Porphyry deposit?

Based on my experience, it is quite rare to find a fertile porphyry that contains only gold. Most porphyry deposits are typically associated with copper. However, Julian informs us that their system at the Northern Zone is devoid of any other metals and is solely a gold system. When we examine the historical drilling results, we can observe significant depth of mineralization, and the grades fall within the range of atypical mineralised porphyry gold system.

Julian has mentioned that they are currently awaiting the results from their recent drilling program. These results will help confirm the assay content and determine if there is any false enrichment present (see below).

It will be fascinating to see the assay numbers and gain a better understanding of the potential of this project. The core samples from the drilling program appear to be in excellent condition, which further adds to the anticipation of the assay results.

Listen to Julian Ford here:

Chapters:

00:00 Start

00:20 Introduction

01:03 Updates from Riversgold

02:57 The Gold Porphyry story

11:22 Metallurgical Cyanide Bottle Roll Test Results

13:37 How did the Northern Zone Project fly under the radar for so long?

19:34 Mt Weld Project

20:54 How should shareholders look at Riversgold?

23:04 Newsflow

23:50 Is the Porphyry story the main focus of Riversgold?

25:26 Why Riversgold?

26:03 Conclusion

Samso's Conclusion

The Riversgold story is an evolving narrative, and I appreciate the adventurous spirit of their projects. Julian impresses me as a composed and strategic individual who possesses a deep understanding of his work. When examining the Northern Zone project, the drilling results are remarkable and align with the expectations for a sizable deposit with low-grade bulk tonnage.

According to theVisual Capitalist,porphyry deposits are very large, polymetallic systems that typically contain copper along with other important metals. Much of today’s mineral production depends on porphyries: 60% of copper, 95% of molybdenum, and 20% of gold comes from this deposit type.

The Bingham Canyon Mine, located in Utah and owned by Rio Tinto and in production since 1906, annually produces approximately:

300,000 tons of copper

400,000 oz of gold

4,000,000 oz of silver

30,000,000 lbs of molybdenum

The value of the resources extracted to date from the Bingham Canyon Mine is greater than theComstock Lode,Klondike, and California gold rush mining regions combined.

So as you can see above, the magnitude of finding a deposit of this nature in a Tier-1 jurisdiction like Western Australia is going to make Riversgold appreciate in market capitalisation.